The question posed in the heading to this post is a scenario that is referenced in the National Directed Trust Act. The following is the short answer for California: under the California Uniform Directed Trust Act a fiduciary trustee director’s conduct and liability can be limited for conduct and culpability that are below the level of willful misconduct (i.e., that do not constitute willful misconduct) if the provisions of the trust so specify, and if the conduct in question is by law within the scope and authority of a trustee director, and if the conduct in question is within the scope and authority of the specific trustee director in question as specified by the terms of the specific directed trust.

Laws, regulations, instruments, and other materials that you may want to consider when evaluating the above issues at least include the following:

– The provisions of the specific directed trust in question.

– In appropriate circumstances and when necessary, the trustor’s intent and wishes.

– The legal definition of willful misconduct.

– The California Uniform Directed Trust Act, including for example new Cal. Probate Code §§16608, 16612, 16614 and 16630 (and perhaps also Probate Code §16618 as related).

– The National Uniform Directed Trust Act including for example Section 8 (Duty and Liability of Trust Director) and Comments thereafter (Extended discretion, and Exculpation or exoneration, and possibility including the Restatement (Third) of Trusts and the Uniform Trust Code).

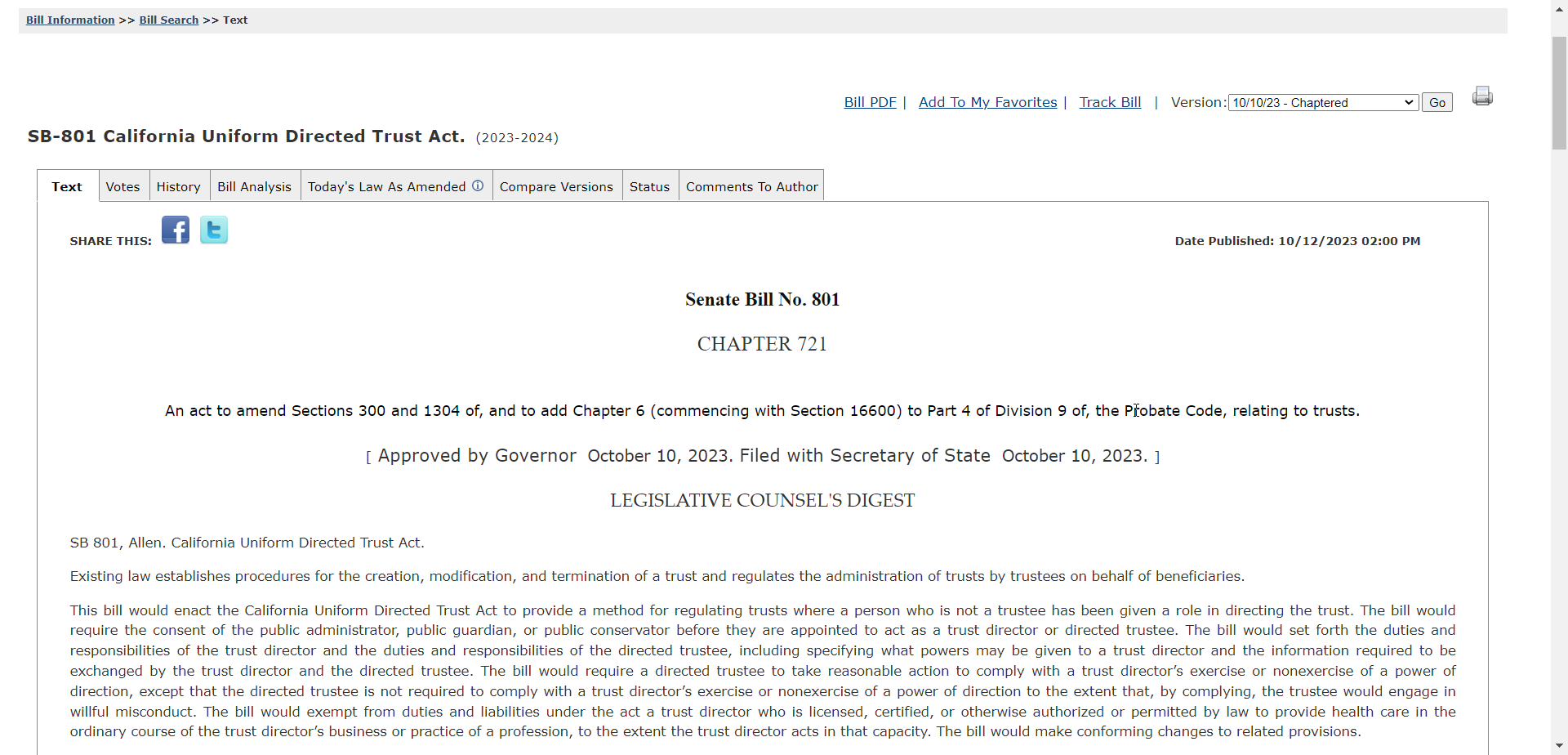

– California Assembly Committee on Judiciary, June 6, 2023, hearing Synopsis which in part states “This bill would enact the California Uniform Directed Trust Act, which, according to the author and co-sponsors, is modeled on the National Commission’s UDTA, but with minor modifications to reflect California law and drafting practices.”

– See also and consider already existing California Probate Code §16461 as relevant to the specific circumstances in question ((b) A provision in the trust instrument is not effective to relieve the trustee of liability (1) for breach of trust committed intentionally, with gross negligence, in bad faith, or with reckless indifference to the interest of the beneficiary, or (2) for any profit that the trustee derives from a breach of trust).

On this blog you will find additional prior posts about the new California directed trusts – additional posts will also be following as I have a list of directed trust scenarios that I will be covering.

* * * *

Thank you for viewing this discussion. Please do pass this blog and blog post and information to other people who would be interested as it is only through collaboration and sharing that great things and success are more quickly achieved. If you are interested in discussing anything that I have said in the discussion above or in either of my two blogs (see blog addresses below), or if you simply want to reach out or are seeking assistance, it is best to reach me by email at dave@tateattorney.com.

David Tate, Esq. (and inactive CPA)

- Business litigation and disputes – business, breach of contract/commercial, co-owners, shareholders, investors, founders, workplace and employment, environmental, D&O, governance, boards and committees.

- Trust, estate and probate court litigation and disputes – trust, estate, probate, elder and dependent abuse, conservatorship, POA, real property, mental health and care, mental capacity, undue influence, conflicts of interest, and contentious administrations.

- Governance, boards, audit and governance committees, investigations, auditing, ESG, etc.

- Mediator and facilitating dispute resolution (evaluative and facilitative):

- Trust, estate, probate, conservatorship, elder and dependent abuse, etc.

- Business, breach of contract/commercial, owner, shareholder, investor, etc.

- D&O, board, audit and governance committee, accountant and CPA related.

- Other: workplace and employment, environmental, trade secret.

Remember, every case and situation is different. It is important to obtain and evaluate all of the evidence that is available, and to apply that evidence to the applicable standards and laws. You do need to consult with an attorney and other professionals about your particular situation. This post is not a solicitation for legal or other services inside of or outside of California, and, of course, this post only is a summary of information that changes from time to time, and does not apply to any particular situation or to your specific situation. So . . . you cannot rely on this post for your situation or as legal or other professional advice or representation, or as or for my opinions and views on the subject matter.

Also note – sometimes I include links to or comments about materials from other organizations or people – if I do so, it is because I believe that the materials are worthwhile reading or viewing; however, that does not mean that I do not or that I might not have a different view about some or even all of the subject matter or materials, or that I necessarily agree with, or agree with everything about or relating to, that organization or person, or those materials or the subject matter.

Please also subscribe to this blog and my other blog (see below), and connect with me on LinkedIn and Twitter.

My two blogs are:

http://tateattorney.com – business, D&O, audit committee, governance, compliance, etc. – previously at http://auditcommitteeupdate.com

Trust, estate, conservatorship, elder and elder abuse, etc. litigation and contentious administrations http://californiaestatetrust.com

David Tate, Esq. (and inactive California CPA) – practicing only as an attorney in California.